What Is Capitalism?

:max_bytes(150000):strip_icc()/cap_v_soc-64336f86820c4217be021540b233461c.jpg)

Capitalism is an economic system characterized by private ownership

Capitalism is an economic system in which private individuals or businesses own capital goods. The production of goods and services is based on supply and demand in the general market—known as a market economy—rather than through central planning—known as a planned economy or command economy.

The purest form of capitalism is free market or laissez-faire capitalism. Here, private individuals are unrestrained. They may determine where to invest, what to produce or sell, and at which prices to exchange goods and services. The laissez-faire marketplace operates without checks or controls.

Today, most countries practice a mixed capitalist system that includes some degree of government regulation of business and ownership of select industries.

Volume 75% 2:05

Capitalism

Understanding Capitalism

Functionally speaking, capitalism is one process by which the problems of economic production and resource distribution might be resolved. Instead of planning economic decisions through centralized political methods, as withsocialism or feudalism, economic planning under capitalism occurs via decentralized and voluntary decisions.

KEY TAKEAWAYS

- Capitalism is an economic system characterized by private ownership of the means of production, especially in the industrial sector.

- Capitalism depends on the enforcement of private property rights, which provide incentives for investment in and productive use of productive capital.

- Capitalism developed historically out of previous systems of feudalism and mercantilism in Europe, and dramatically expanded industrialization and the large-scale availability of mass-market consumer goods.

- Pure capitalism can be contrasted with pure socialism (where all means of production are collective or state-owned) and mixed economies (which lie on a continuum between pure capitalism and pure socialism).

- The real-world practice of capitalism typically involves some degree of so-called “crony capitalism” due to demands from business for favorable government intervention and governments’ incentive to intervene in the economy.

Capitalism and Private Property

Private property rights are fundamental to capitalism. Most modern concepts of private property stem from John Locke’s theory of homesteading, in which human beings claim ownership through mixing their labor with unclaimed resources. Once owned, the only legitimate means of transferring property are through voluntary exchange, gifts, inheritance, or re-homesteading of abandoned property.

Private property promotes efficiency by giving the owner of resources an incentive to maximize the value of their property. So, the more valuable the resource is, the more trading power it provides the owner. In a capitalist system, the person who owns the property is entitled to any value associated with that property.

For individuals or businesses to deploy their capital goods confidently, a system must exist that protects their legal right to own or transfer private property. A capitalist society will rely on the use of contracts, fair dealing, and tort law to facilitate and enforce these private property rights.

When a property is not privately owned but shared by the public, a problem known as the tragedy of the commons can emerge. With a common pool resource, which all people can use, and none can limit access to, all individuals have an incentive to extract as much use value as they can and no incentive to conserve or reinvest in the resource. Privatizing the resource is one possible solution to this problem, along with various voluntary or involuntary collective action approaches.

Capitalism, Profits, and Losses

Profits are closely associated with the concept of private property. By definition, an individual only enters into a voluntary exchange of private property when they believe the exchange benefits them in some psychic or material way. In such trades, each party gains extra subjective value, or profit, from the transaction.

Voluntary trade is the mechanism that drives activity in a capitalist system. The owners of resources compete with one another over consumers, who in turn, compete with other consumers over goods and services. All of this activity is built into the price system, which balances supply and demand to coordinate the distribution of resources.

A capitalist earns the highest profit by using capital goods most efficiently while producing the highest-value good or service. In this system, information about what is highest-valued is transmitted through those prices at which another individual voluntarily purchases the capitalist’s good or service. Profits are an indication that less valuable inputs have been transformed into more valuable outputs. By contrast, the capitalist suffers losses when capital resources are not used efficiently and instead create less valuable outputs.

Free Enterprise or Capitalism?

Capitalism and free enterprise are often seen as synonymous. In truth, they are closely related yet distinct terms with overlapping features. It is possible to have a capitalist economy without complete free enterprise, and possible to have a free market without capitalism.

Any economy is capitalist as long as private individuals control the factors of production. However, a capitalist system can still be regulated by government laws, and the profits of capitalist endeavors can still be taxed heavily.

“Free enterprise” can roughly be understood to mean economic exchanges free of coercive government influence. Although unlikely, it is possible to conceive of a system where individuals choose to hold all property rights in common. Private property rights still exist in a free enterprise system, although the private property may be voluntarily treated as communal without a government mandate.

Many Native American tribes existed with elements of these arrangements, and within a broader capitalist economic family, clubs, co-ops, and joint-stock business firms like partnerships or corporations are all examples of common property institutions.

If accumulation, ownership, and profiting from capital is the central principle of capitalism, then freedom from state coercion is the central principle of free enterprise.

Feudalism the Root of Capitalism

Capitalism grew out of European feudalism. Up until the 12th century, less than 5% of the population of Europe lived in towns. Skilled workers lived in the city but received their keep from feudal lords rather than a real wage, and most workers were serfs for landed nobles. However, by the late Middle Ages rising urbanism, with cities as centers of industry and trade, become more and more economically important.

The advent of true wages offered by the trades encouraged more people to move into towns where they could get money rather than subsistence in exchange for labor. Families’ extra sons and daughters who needed to be put to work, could find new sources of income in the trade towns. Child labor was as much a part of the town’s economic development as serfdom was part of the rural life.

Mercantilism Replaces Feudalism

Mercantilism gradually replaced the feudal economic system in Western Europe and became the primary economic system of commerce during the 16th to 18th centuries. Mercantilism started as trade between towns, but it was not necessarily competitive trade. Initially, each town had vastly different products and services that were slowly homogenized by demand over time.

After the homogenization of goods, trade was carried out in broader and broader circles: town to town, county to county, province to province, and, finally, nation to nation. When too many nations were offering similar goods for trade, the trade took on a competitive edge that was sharpened by strong feelings of nationalism in a continent that was constantly embroiled in wars.

Colonialism flourished alongside mercantilism, but the nations seeding the world with settlements were not trying to increase trade. Most colonies were set up with an economic system that smacked of feudalism, with their raw goods going back to the motherland and, in the case of the British colonies in North America, being forced to repurchase the finished product with a pseudo-currency that prevented them from trading with other nations.

It was Adam Smith who noticed that mercantilism was not a force of development and change, but a regressive system that was creating trade imbalances between nations and keeping them from advancing. His ideas for a free market opened the world to capitalism.

Growth of Industrial Capitalism

Smith’s ideas were well-timed, as the Industrial Revolution was starting to cause tremors that would soon shake the Western world. The (often literal) gold mine of colonialism had brought new wealth and new demand for the products of domestic industries, which drove the expansion and mechanization of production. As technology leaped ahead and factories no longer had to be built near waterways or windmills to function, industrialists began building in the cities where there were now thousands of people to supply ready labor.

Industrial tycoons were the first people to amass their wealth in their lifetimes, often outstripping both the landed nobles and many of the money lending/banking families. For the first time in history, common people could have hopes of becoming wealthy. The new money crowd built more factories that required more labor, while also producing more goods for people to purchase.

During this period, the term “capitalism”—originating from the Latin word “capitalis,” which means “head of cattle”—was first used by French socialist Louis Blanc in 1850, to signify a system of exclusive ownership of industrial means of production by private individuals rather than shared ownership.

Contrary to popular belief, Karl Marx did not coin the word “capitalism,” although he certainly contributed to the rise of its use.

Industrial Capitalism’s Effects

Industrial capitalism tended to benefit more levels of society rather than just the aristocratic class. Wages increased, helped greatly by the formation of unions. The standard of living also increased with the glut of affordable products being mass-produced. This growth led to the formation of a middle class and began to lift more and more people from the lower classes to swell its ranks.

The economic freedoms of capitalism matured alongside democratic political freedoms, liberal individualism, and the theory of natural rights. This unified maturity is not to say, however, that all capitalist systems are politically free or encourage individual liberty. Economist Milton Friedman, an advocate of capitalism and individual liberty, wrote in Capitalism and Freedom (1962) that “capitalism is a necessary condition for political freedom. It is not a sufficient condition.”

A dramatic expansion of the financial sector accompanied the rise of industrial capitalism. Banks had previously served as warehouses for valuables, clearinghouses for long-distance trade, or lenders to nobles and governments. Now they came to serve the needs of everyday commerce and the intermediation of credit for large, long-term investment projects. By the 20th century, as stock exchanges became increasingly public and investment vehicles opened up to more individuals, some economists identified a variation on the system: financial capitalism.

Capitalism and Economic Growth

By creating incentives for entrepreneurs to reallocate away resources from unprofitable channels and into areas where consumers value them more highly, capitalism has proven a highly effective vehicle for economic growth.

Before the rise of capitalism in the 18th and 19th centuries, rapid economic growth occurred primarily through conquest and extraction of resources from conquered peoples. In general, this was a localized, zero-sum process. Research suggests average global per-capita income was unchanged between the rise of agricultural societies through approximately 1750 when the roots of the first Industrial Revolution took hold.

In subsequent centuries, capitalist production processes have greatly enhanced productive capacity. More and better goods became cheaply accessible to wide populations, raising standards of living in previously unthinkable ways. As a result, most political theorists and nearly all economists argue that capitalism is the most efficient and productive system of exchange.

Capitalism vs. Socialism

In terms of political economy, capitalism is often pitted against socialism. The fundamental difference between capitalism and socialism is the ownership and control of the means of production. In a capitalist economy, property and businesses are owned and controlled by individuals. In a socialist economy, the state owns and manages the vital means of production. However, other differences also exist in the form of equity, efficiency, and employment.

Equity

The capitalist economy is unconcerned about equitable arrangements. The argument is that inequality is the driving force that encourages innovation, which then pushes economic development. The primary concern of the socialist model is the redistribution of wealth and resources from the rich to the poor, out of fairness, and to ensure equality in opportunity and equality of outcome. Equality is valued above high achievement, and the collective good is viewed above the opportunity for individuals to advance.

Efficiency

The capitalist argument is that the profit incentive drives corporations to develop innovative new products that are desired by the consumer and have demand in the marketplace. It is argued that the state ownership of the means of production leads to inefficiency because, without the motivation to earn more money, management, workers, and developers are less likely to put forth the extra effort to push new ideas or products.

Employment

In a capitalist economy, the state does not directly employ the workforce. This lack of government-run employment can lead to unemployment during economic recessions and depressions. In a socialist economy, the state is the primary employer. During times of economic hardship, the socialist state can order hiring, so there is full employment. Also, there tends to be a stronger “safety net” in socialist systems for workers who are injured or permanently disabled. Those who can no longer work have fewer options available to help them in capitalist societies.

Mixed System vs. Pure Capitalism

When the government owns some but not all of the means of production, but government interests may legally circumvent, replace, limit, or otherwise regulate private economic interests, that is said to be a mixed economy or mixed economic system. A mixed economy respects property rights, but places limits on them.

Property owners are restricted with regards to how they exchange with one another. These restrictions come in many forms, such as minimum wage laws, tariffs, quotas, windfall taxes, license restrictions, prohibited products or contracts, direct public expropriation, anti-trust legislation, legal tender laws, subsidies, and eminent domain. Governments in mixed economies also fully or partly own and operate certain industries, especially those considered public goods, often enforcing legally binding monopolies in those industries to prohibit competition by private entities.

In contrast, pure capitalism, also known as laissez-faire capitalism or anarcho-capitalism, (such as professed by Murray N. Rothbard) all industries are left up to private ownership and operation, including public goods, and no central government authority provides regulation or supervision of economic activity in general.

The standard spectrum of economic systems places laissez-faire capitalism at one extreme and a complete planned economy—such as communism—at the other. Everything in the middle could be said to be a mixed economy. The mixed economy has elements of both central planning and unplanned private business.

By this definition, nearly every country in the world has a mixed economy, but contemporary mixed economies range in their levels of government intervention. The U.S. and the U.K. have a relatively pure type of capitalism with a minimum of federal regulation in financial and labor markets—sometimes known as Anglo-Saxon capitalism—while Canada and the Nordic countries have created a balance between socialism and capitalism.

Many European nations practice welfare capitalism, a system that is concerned with the social welfare of the worker, and includes such policies as state pensions, universal healthcare, collective bargaining, and industrial safety codes.

Crony Capitalism

Crony capitalism refers to a capitalist society that is based on the close relationships between business people and the state. Instead of success being determined by a free market and the rule of law, the success of a business is dependent on the favoritism that is shown to it by the government in the form oftax breaks, government grants, and other incentives.

In practice, this is the dominant form of capitalism worldwide due to the powerful incentives both faced by governments to extract resources by taxing, regulating, and fostering rent-seeking activity, and those faced by capitalist businesses to increase profits by obtaining subsidies, limiting competition, and erecting barriers to entry. In effect, these forces represent a kind of supply and demand for government intervention in the economy, which arises from the economic system itself.

Crony capitalism is widely blamed for a range of social and economic woes. Both socialists and capitalists blame each other for the rise of crony capitalism. Socialists believe that crony capitalism is the inevitable result of pure capitalism. On the other hand, capitalists believe that crony capitalism arises from the need of socialist governments to control the economy.

- Published in Articles

How a Population of 4.2 Billion Could Impact Africa by 2100:

The Possible Economic, Demographic, and Geopolitical Outcomes

Background

For better or worse, population growth in Africa over the next three decades will change the course of human history. The continent is currently home to 1.3 billion people, equal to roughly 17 percent of the world’s total population.[1] By 2050, Africa’s population will increase to an unprecedented 2.4 billion and eventually to a staggering 4.2 billion by 2100.[2] The continent will nearly become the most populated on earth—trailing only Asia’s 4.8 billion.

Many Sub-Saharan African countries will thus figure amongst the most highly populated in the world. Africa’s most populous country, Nigeria, whose population of 190 million people is currently growing at 3 percent annually, will have more than 400 million people by 2050.[3] The Democratic Republic of Congo—currently 81 million—will have 195 million. Ethiopia, which currently sits at 105 million, will reach 188 million. Tanzania, currently at 57 million, and Uganda, currently at 42 million, will also experience remarkable surges—similar to Nigeria’s—with 129 million and 101 million people respectively by 2050. These are all enormous numbers that portend massive challenges for a continent that is already struggling to provide for its current population of 1.3 billion. As African countries face down this looming demographic explosion, there are several critical questions economists are attempting to answer.

The Pressing Questions

Economists are divided on whether Africa’s population growth will indeed reach the UN’s predicted 2.4 billion and 4.2 billion population levels by 2050 and 2100, respectively. Those who subscribe to the UN’s prediction often reference the persistent upward growth of the continent’s population since the mid 20thcentury. Since 1982 Africa’s population has more than doubled with the continent passing the 1 billion mark in 2009. Meanwhile, between 2011 and 2015, Africa’s population growth rate averaged 2.55 percent annually—the highest in the world.Economists believe the decrease in infant mortality rate coupled with the reduction in deaths from diseases like malaria, cholera, and hopefully soon, AIDS, points to the plausibility of the UN’s predictions.

Skeptics, while recognizing past growth trends, do not believe the trends will peak as high as the UN projects, particularly in light of possible future political, health, and climatic changes that they argue are not comprehensively accounted for in UN calculations. Although there is a strong possibility of unforeseen factors slowing down the population growth rate, the UN’s population predictions still appear highly realistic.[4] A closer look at Africa’s demography further validates the UN’s projections.

Nearly all of the countries in Africa have a sex ratio skewed in favor of females. More significantly, though, they all have an overwhelmingly youthful population, specifically below age 15.[5] In conventional demography, a predominantly youthful and female-dominated population often portends an increasing birth rate. In Africa, this general pattern may even be exacerbated as use of contraceptives and access to family planning services are severely limited.Anincreasing birth rate will also produce a larger youth population in successive decades. This again points to the possibility of a sustained, high future growth rate, as John Wilmoth, Director of the Population Division at the United Nations corroborates, stating: “41 percent of the [continent’s] population is under the age [of] 15. This is a very high fraction. Another 19 percent are between ages 15 and 24. So if you add those two together you’ve got three-fifths of the population that is under the age of 25.”[6]

Some economists have argued that this radical increase in population will plunge the continent into further economic misery. They believe that much of the new population will fall into the extreme poverty bracket, especially if critical infrastructure related to things like health, security, and education remain poor over the coming decades. On the other hand, optimists believe this demographic explosion could, in fact, be propitious for Africa’s economic growth prospects. Such a population increase could enable Africa to undergo an industrial revolution, if the continent can adapt and implement proper economic policies, learning from the examples of China and India.[7]

The total fertility rate by world region including the UN projections through 2100. Source: OurWorldInData.org/future-population-growth/

But Africa’s roadmap to 2050 and 2100 is far from clear. As such, a comprehensive evaluation of plausible outcomes and opportunities is necessary for African leaders to make informed judgments on what policies to pursue. Thus, the key question here is not if the continent is ready for the ensuing demographic change, but how it will manage the change.

Significant Changes to Anticipate in the Coming Decades

Unprecedented Pressure on Infrastructure

Africa’s infrastructure gap will take around $170 billion annually to fill.[8] This is perhaps the most frequently cited statistic about Africa among development economists after the UN’s “2.4 billion population increase by 2050” prediction, and rightly so. It is a troubling reality if put in the context of how difficult it will be for the continent to finance. It is, though, a reality that some African leaders are attempting to come to terms with.

In the immediate years following their independence, many African governments made strenuous efforts to invest in critical infrastructure, often using proceeds generated from nationalized assets inherited from the colonial period and, in some cases, bolstered by foreign aid and loans. Although this building spree created some of the most enduring infrastructure across the continent, it fell well short of meeting the demands of the fast-growing continent. Indeed, the infrastructure gap the UN and others are deeply concerned over actually began to worsen in the 1980s and 1990s when civil wars and coups destabilized many countries. This underinvestment in infrastructure has, at the same time, been exacerbated by the concomitant rise in systemic corruption. During these two decades, many countries that were not economically destabilized also watched as their infrastructure gaps widened in the hands of corrupt governments. The gap grew even larger in the 1990s and throughout the first decade of the millenniumdespite the fact that Africa had more loans and foreign aid to help address the problem than in any period prior.

A 2013 joint report by the AfDB and Global Financial Integrity claimed that about$1.3 trillion was taken from Africa in illicit financial flows between 1980 and 2009, which is roughly equivalent to Africa’s GDP for 2014.[9] Back in 2002, the African Union revealed that the continent loses about $150 billion annually to corruption. More recently, in 2018, the United Nations Economic Commission for Africa estimated the annual losses to corruption through fraudulent activities to be around $148 billion—about 5 percent of the continent’s average GDP. This means if the continent can fix the loopholes through which state funds are corruptly mismanaged, Africa would have almost the equivalent of its annual infrastructure expenses. Meanwhile, African leaders have turned to international creditors like the AfDB, the World Bank, the International Monetary Fund, the European Union, and lately, China to finance these expenses. But the expedient route of relying on loans while continuing to forego the lost revenue from corruption is not sustainable over the long-term. Fixing the corruption problem is a sustainable, internal alternative to generate the revenue necessary for infrastructure development.

The challenge of accommodating an additional 2.4 billion people, let alone 4.2 billion, will be nearly insurmountable if the ratio of basic infrastructure to individual does not radically improve over the next few decades. As Africa as a whole struggles with this, urban centers like Nairobi, Kampala, Lagos, Kinshasa, and others—most of which are already poorly built—will become the center of infrastructure pressure as Africa increasingly urbanizes. Hospitals will grow increasingly overcrowded whilemillions of new commuters will pack major roads that are hardly robust enough to accommodate their current user base. Other critical infrastructure, in particular security and energy, remains inadequate in these cities, and will, if unaddressed, contribute to dysfunction. In order for Africa to avert this looming problem, there must be sufficient investment in infrastructure. But meeting the $170 billion annual threshold set by the African Development Bank Group (AfDB) will be extremely difficult, especially as the continent continues to lose potential resources to corruption.

Expanding Labor Force

Africa’s labor force is currently among the largest in the world and it will soon be the largest. Africa couldbenefit from this unprecedented increase in its labor force. Indeed, this would ordinarily strengthen economies and governments by increasing both labor supply and taxable income. In Africa, though, there will be a tremendous amount of pressure on governments to design policies that will allow the economy to produce new jobs and meet the needs of a growing labor force. Unfortunately, African leaders are currently failing in this regard. They should prioritize the creation of an environment that will attract foreign direct investment, including a reduction in corporate tax and minimal regulations on businesses, especially for small and medium-sized enterprises. Thebenefits of creating a stable, effective, and non-cumbersome business environment are likely to be substantial. It could make Africa the next bastion of cheap and abundant labor for multinational corporations, in direct competition with China and India.

The best way for African leaders to initiate this opportunity is by helping to make the incoming labor force skilled and educated enough to compete with those of both China and India, or to at least match their level of competitiveness. A strong initial step could be a massive investment in technical education over the next few decades.

A New African Middle Class

The population of Africa’smiddle class has significantly increased over the last five decades and will likely continue to do so. The AfDB estimated in 2011 that Africa’s middle-class population had risen from 126 million(27 percent of the continent’s population) in 1980 to about 350 million in 2010(roughly 34 percent of that year’s 1 billion population). A Brookings Institution study found that “582 million Africans will have estimated revenues of $2 to $20 a day [by 2030], classing them in the middle class. An additional 116 million people will have revenues higher than $20 a day, for a total of 698 million people from the middle and upper classes.” The study further found that while in 2013 the middle and upper classes represented only 33.90 percent of the population, “in 2030, [they are] estimated to represent about 42.69 percent of the population.”[10]

This is a promising prediction for Africa. Middle class growth of roughly 9 percent within seventeen years (2013 to 2030 as calculated by the Brookings Institution) would be a positive change for any serious economy. Meanwhile, disposable income will similarly improve. There will be 56 million middle-class households with disposable incomes of nearly $680 billion by 2030 in Africa. A growing population with increasing incomes means there will be more money for Africans to spend, save, and invest. Indeed, the same Brookings report claimed that consumerexpenditure on the continent had grown from “a compound annual rate of 3.9 percent since 2010 and reached $1.4 trillion in 2015,” and that the “figure is expected to reach $2.1 trillion by 2025, and $2.5 trillion by 2030.” African countries can use this consumption-based economic growth, fueled by the middle class, to their advantage.[11]

A Larger Consumer Market

China’s status as the second-largest consumer market in the world has much to do with the substantial personal income of its 788 million labor force. Africa too, over the coming decades, could develop as a major consumer market powered by its labor force. Population growth in Africa—as indicated earlier—will measure at rates of 25 percent in 2050 and 39 percent by 2100. Whereas in Asia, the rate will fall from 54 percent in 2050 to 44 percent by 2100. At the same time, the fertility rates in Africa and Asia respectively are 4.5 and 2.1 children on average, and these rates will likely remain relatively unchanged for both continents for at least the next two decades.[12] Macroeconomic thought holds that market opportunities in highly-populated economies are usually greater than those in lowly populated economies. This is based upon the notion that the more potential consumers within an economy, the more demand there is for goods and services. If the personal income rate in an economy grows as quickly as the population, then this will create an even larger consumer market.

As we have seen historically, corporations will go to great lengths to expand and tap into highly populated consumer markets like those of China, India, the United States, and Brazil. Yet, while corporations certainly profit, there is perhaps an even bigger benefit for the host countries. When a company plans to introduce its product into a new market, there are taxes, import duties, and other forms of royalties that governments usually impose as means of generating revenue. The larger the demand and purchasing power of a given population, the more investment interest there is, and hence the larger the size of possible revenue from state royalties. A related outcome will be an increase in job opportunities, as the increase in investments leads to greater demand for labor. As corporations enter into new markets, they invariably require local labor, which provides openings to the middle class and increases the tax base.

Possible Geopolitical Outcomes

A Possible Shift in Economic Power

Global GDP currently stands at a staggering $80 trillion in nominal terms with almost 40 percent of it attributable to the United States and China. The largest African countries, Nigeria and South Africa, account for just 0.47 percent and 0.44 percent of global GDP respectively. If the three changes identified above (the growth of the middle class, fostering a competitive labor force, and developing a large consumer market) were to yield the predicted results, there is a good chance that the GDP of a few major African economies could jump into the top 10 by 2050.

An Increase in Global Poverty Rate and Migration

Many governments experiencing a high population growth rate face the often concomitant problem of reducing poverty. For African countries especially, this task will be daunting. The global poverty rate has dropped in recent years, especially with the rise of China and India. Sub-Saharan Africa, on the other hand, is now home to more than half of the world’s extreme poor. Over 413 million people in the region live in extreme poverty—mostly in countries like Nigeria, the Democratic Republic of Congo and Uganda, which will all experience the largest increase in population. At the same time, most of the countries with the highest unemployment rates in the world are in Africa.[13] Senegal (48 percent) and Djibouti (40 percent) are among the worst in the world,[14] while stronger economies like South Africa (27 percent)[15] and Nigeria (23 percent)[16] are still struggling mightily with unemployment as well. As a result, out of the 420 million young Africans aged 15 to 35, one-third are unemployed and another third are vulnerably employed with only one out of every six of Africa’s youth in wage employment.[17] The World Bank predicts that if African governments do not quickly and sufficiently build out infrastructure to both stimulate and accommodate job creation, 9 out of 10 of the world’s extreme poor will be in Sub-Saharan Africa by 2030.

If the economic situation of these African countries does not improve as we approach 2050, the rate of emigration from Africa will likely skyrocket well beyond current figures. Africa’s outlook over the next two decades is already fraught. Finding jobs for the rapidly expanding younger demographic—which is the core of the labor force distribution—will be a huge task. Indeed, many have shown the link between factors like financial insecurity and unemployment to the mass exodus of Africans across the Mediterranean Sea to the coasts of Europe. If there are more people without jobs living in weak economies in Sub-Saharan Africa in the coming decades, greater numbers of people will attempt to leave.

Conclusion

As 2050 draws near, African leaders must quickly acknowledge the scope of the demographic challenge and begin implementing the right policies to buttress their countries against it. Should African leaders fail to properly prepare, Africa is at risk of descending into a full-blown humanitarian crisis. Fortunately for African leaders, there are precedents to learn from, namely China and India.

Indeed, it is important that low-income countries not copy the development model of higher-income countries outright. For Africa, then, similar policies that helped both China and India in managing their population surges are replicable. These include such things as mitigating corruption, liberalization of economies, investing in labor force competitiveness (especially in the field of information technology) and creating an attractive business environment.

In the interim, every African country must initiate sustainable frameworks to fix its infrastructure gaps. This will likely not be achieved through heavy state borrowing; Africa does not have a good history of loan servicing or debt management. Instead, African leaders should consider how state revenue from trade and other means can be judiciously used to raise the necessary funds for infrastructure development to accommodate the imminent population growth. The looming change in the continent’s demography requires careful evaluation and the policies must be well informed. For Africa, the risk in doing nothing could yield consequences almost as great as doing the wrong thing.

References

[1]“World Population Prospects: United Nations’ 2017 edition of World Population Prospects.” United Nations.

- Published in News

The fastest growing cities in the world

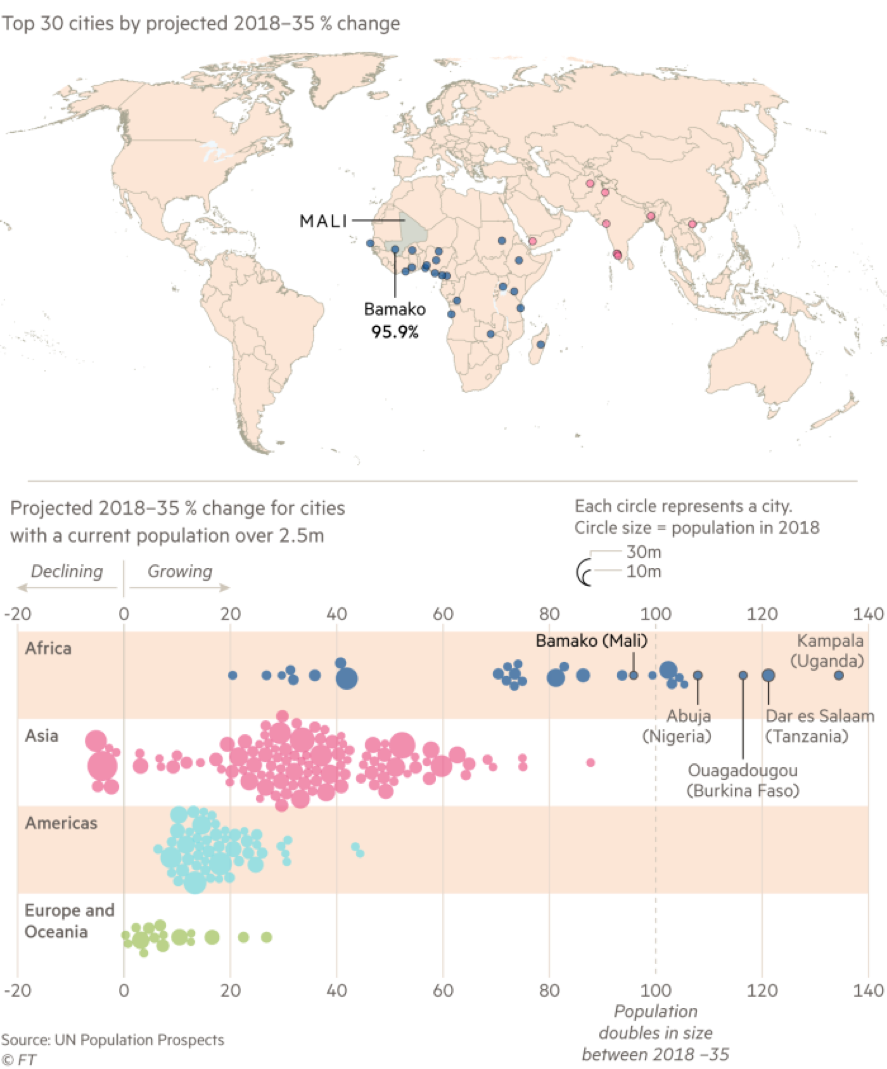

The United Nations Department of Economic and Social Affairsprojects that the world’s 10 fastest growing cities, between 2018 and 2035, will all be in Africa. The visualization below first maps the location of the fastest growing cities in the world with a population greater than 2.5 million. Interestingly, many of the fastest growing African cities are specifically located on the Gulf of Guinea including Lagos, Abuja, Abidjan, Doula, and Kumasi.

While Africa only has a handful of large, urban agglomerations when compared to places like Asia and the Americas, as the bottom half of Figure 1 shows, Africa will host eight cities that are expected to more than double in population size in the next 17 years. In fact, most of these large African cities are growing faster than all other big cities in the world.

Among the other top 30 are Mumbai in India, Dhaka in Bangladesh, Sana’a in Yemen, and Hanoi in Vietnam. The 2018 Revision of the World Urbanization Prospects also finds that just three countries—India, China, and Nigeria—together are expected to account for 35 percent of the growth in the world’s urban population between 2018 and 2050. Nigeria alone is projected to add 189 million urban dwellers.

Growth in the urban population is driven by a combination of overall population increase and an upward shift in the percentage of people living in urban areas. Together, these factors are projected to add 2.5 billion people to the world’s urban population by 2050 with 90 percent of this growth happening in Asia and Africa. Policymakers from around the world are under pressure to address these immense demographic changes and accompanying urban challenges.

Figure 1: Of the world’s 30 fastest-growing cities, 21 are in Africa

- Published in News

Create an Effective Business Strategy

Stepping forward into the unknown (also known as ‘the future’) is what companies do every day.

And what do they need to make sure they don’t get lost? A strategy, of course, which some may also call a roadmap.

Whether you’re looking to set new business priorities, outline plans for growth, determine a product roadmap or plan your investment decisions, you’ll need a strategy. Coming to the realisation that your organisation needs one is easy. Actually creating a strategy is a little trickier.

Here are six simple steps to help you deliver an effective business strategy:

- Gather the facts

To know where you’re heading, you have to know where you are right now. So before you start looking ahead, you should review the past performance, or the current situation. Look at each area of the business and determine what worked well, what could have been better and what opportunities lie ahead.

There are many tools and techniques available to help with this process, such as SWOT (Strength, Weakness, Opportunities and Threats) analysis.

You should look internally at your strengths and weaknesses. And for the opportunities and threats you should look at external factors. A great framework for looking at external factors is PESTLE (Political, Economic, Social, Technological, Legal and Environmental). So, for your big idea or plan you would ask: what threats and opportunities could arise under each category?

The most important part of this process is involving the right people to make sure you’re collecting the most relevant information.

- Develop a vision statement

This statement should describe the future direction of the business and its aims in the medium to long term. It’s about describing the organisation’s purpose and values. Business gurus have debated long and hard about what comes first – the vision, or the mission statement (see step 3). But, in practice, you could develop both at the same time. - Develop a mission statement

Like the vision statement, this defines the organisation’s purpose, but it also outlines its primary objectives. This focuses on what needs done in the short term to realise the long term vision. So, for the vision statement, you may want to answer the question: “Where do we want to be in 5 years?”. For the mission statement, you’ll want to ask the questions:

What do we do?

How do we do it?

Whom do we do it for?

What value do we bring?

- Identify strategic objectives

At this stage, the aim is to develop a set of high-level objectives for all areas of the business. They need to highlight the priorities and inform the plans that will ensure delivery of the company’s vision and mission.

By taking a look back at your review in step one, in particular the SWOT and PESTLE analysis, you can incorporate any identified strengths and weaknesses into your objectives.

Crucially, your objectives must be SMART (Specific, Measurable, Achievable, Realistic and Time-related). Your objectives must also include factors such as KPI’s, resource allocation and budget requirements.

- Tactical Plans

Now is the time to put some meat on the bones of your strategy by translating the strategic objectives into more detailed short-term plans. These plans will contain actions for departments and functions in your organisation. You may even want to include suppliers.

You’re now focusing on measurable results and communicating to stakeholders what they need to do and when. You can even think of these tactical plans as short sprints to execute the strategy in practice.

- Performance Management

All the planning and hard work may have been done, but it’s vital to continually review all objectives and action plans to make sure you’re still on track to achieve that overall goal. Managing and monitoring a whole strategy is a complex task, which is why many directors, managers and business leaders are looking to alternative methods of handling strategies. Creating, managing and reviewing a strategy requires you to capture the relevant information, break down large chunks of information, plan, prioritise, capture the relevant information and have a clear strategic vision.

- Published in News

How To Find A Mentor And Make It Work

Finding A Mentor

The right mentoring relationship can be a powerful tool for professional growth — it can lead to a new job, a promotion or even a better work-life balance.

One of the trickiest things about mentoring though, is that it’s often informal, and that can make it difficult to find an entry point.

Here’s how to find a good mentor, make the ask and make it work (formally).

1. Finding the Right Mentor

Know your goals (both short and long term). What do you want to accomplish professionally in the next three months? Can you do it in your current role or will it require you to switch jobs? The more specific you are with your goals, the easier it will be to find the right mentor. One strategy to create effective, easily achievable goals is to work SMART: specific, measurable, achievable, relevant, and timebound. Envisioning your dreams this way allows you to break down lofty ideas into individual goals that are easier to accomplish through short-term steps.Article continues after sponsor message

Who do you look up to? Whose job would you like to have in the next 5, 10 or 15 years? Is this person inside or outside your workplace? Who is your immediate role model where you work? Keep a running list of the jobs and people you are visualizing. Consider an identity-based mentor in your organization, especially if you need to talk about issues you’re facing as an underrepresented person in your professional surroundings.

Do the research. You may or may not be able to ask one of those people to be your mentor, but what are the stepping stones to get to someone in a similar position? Take notes on the path that person took to get to where they are today.

Be cognizant of your existing network. The more aware someone already is of your work and abilities, the more effective they will be at mentoring you. Think about whether someone is already informally mentoring you — can you ask them to help you? If someone isn’t aware of your work or you’ve never talked to them, look for a connection. Make sure the person you are thinking about also has the expertise you’re looking for. (We’ll talk more about this in the next section.)

Recognize the difference between a mentor and a sponsor.For example, mentors give advice on but can’t give you the new job, raise, or promotion. In contrast, sponsors can do that for you. They can be a boss, recruiter, or even employer in a new industry. Don’t expect mentors to be sponsors, but they can put you in touch with sponsors. Mentors can also be in your life for the long-term, while sponsors are often more short-term.

Rene Sanchez/NPR

2. Making the Ask

Have an elevator pitch ready.Be clear of your goals and why you think this person is the right mentor for you. Be up front about your time-commitment, what you’re willing to put into the relationship and what you expect from them. If you’re clear about what you need from the start, communication will flow smoothly. You can even practice this elevator pitch to other people before asking the possible mentor.

Make sure it’s the right fit before asking. You can feel this out by having informal meetings where you discuss your goals and trajectory, before asking them to be your mentor.

Mention what you like about the person’s work, especially if you’ve never met. Say your boss introduced you to a possible mentor and neither of you know each other. Do the research about the possible mentor’s work. Then open with what you like about their work. That will show that you have a thoughtful approach.

If it’s a cold email, it’s okay to start with the informational interview ask.But again, be specific about what you like about the person’s work and why you want to meet. Why is talking to you worth their time? If you’ve never met before, consider starting with a phone call and work with the person’s schedule. Keep in mind that informational interview requests are common. The way you stand out, as we mentioned before, is showing you did the research about their career and being specific and honest about what you’re asking of them.

Try to ask for formal mentorship in-person. This isn’t always possible, but when you feel someone is the right fit, do your best to meet in-person to make the ask. It shows that you will be open to feedback in the long term.

Whether it’s in-person or via email, here are some things to mention:

- Tell them specifically what you’ve gotten out of past conversations with them. (This might be from that first informal meeting.)

- Be clear about how often you want to meet for and how long, and make sure it works for them. (You can reassess this later in the relationship.)

- Mention you’ll put together agendas prior to each meeting that align with the goals discussed above.

- Finally, make sure they are considering this mentorship as an option and not an obligation. We’re all busy, and you should approach the ask fully aware they might say no. And that’s okay! If they do say no, mention you admire their path and thank them for considering. That leaves the door open for a future relationship.

3. Tips on Being a Good Mentee

So you’ve found the right mentor. Now what?

Goals still matter. If you mention your specific, achievable goals from the beginning of the relationship, your mentor can help you stay on track at each meeting.

Meet consistently. Figure out how often (i.e. once a week or once a month over four to six months), how long (i.e. half hour or one hour) and how you want to meet and make it consistent. In-person or over video conference is a good start so that you can get to know each other better. Gradually progress to phone calls once you’re comfortable. Decide whether you or your mentor want to send out calendar invites to protect the time you plan to meet. This might mean keeping your supervisor in the loop.

Set an agenda.Before each meeting, send your mentor an agenda — a piece you may want to read with your mentor, a new project you’ve worked on and want feedback on or indicate that you’re trying to ask for a promotion or raise.

Be open to feedback: positive or constructive.Sometimes it can be hard to take a compliment or look back and appreciate your own work. In the same vein, be open to hearing tough feedback.

Take notes as you’re meeting so that you can follow up via email. That will help a busy mentor stay on track and know what to focus on with you over the course of your relationship.

Decide on an end date.Based on how long those short-term goals will take to achieve, decide how long you want the mentorship relationship to last. A good rule of thumb is usually four to six months, with the option to keep meeting informally.

This relationship is not a therapy session. Remember to make and keep boundaries. We are human, and often personal issues will come into play during your sessions, especially if you have a pre-existing relationship or are talking about work-life balance. It’s okay to vent. But make sure not to monopolize the session with personal issues or make it only about venting.

Finally, consider establishing a board of mentors.No one mentor can help you achieve all of your goals. Maybe one mentor can help you consider a path to leadership because they are a supervisor. Maybe another can help with technical skills specific to making a job change. Another mentor may be aware of your skill set and could turn into a sponsor down the line. There is no right or wrong number of mentors as you progress through your professional career. Even if a formal mentorship period ends, keep these mentors in your life and updated of your achievements and pitfalls. They can be a guide when you’re unsure and will feel appreciated that they helped you get to the place you’re at in your career. Win-win!

- Published in News

What is mentoring?

Personal and Professional Development

Mentoring is a system of semi-structured guidance whereby one person shares their knowledge, skills and experience to assist others to progress in their own lives and careers. Mentors need to be readily accessible and prepared to offer help as the need arises – within agreed bounds.

Mentors very often have their own mentors, and in turn their mentees might wish to ‘put something back’ and become mentors themselves – it’s a chain for ‘passing on’ good practice so that the benefits can be widely spread.

Mentoring can be a short-term arrangement until the original reason for the partnership is fulfilled (or ceases), or it can last many years.

Mentoring is more than ‘giving advice’, or passing on what your experience was in a particular area or situation. It’s about motivating and empowering the other person to identify their own issues and goals, and helping them to find ways of resolving or reaching them – not by doing it for them, or expecting them to ‘do it the way I did it’, but by understanding and respecting different ways of working.

Mentoring is not counselling or therapy – though the mentor may help the mentee to access more specialised avenues of help if it becomes apparent that this would be the best way forward.

What’s in it for you?

As mentee

Being able to change/achieve your goals more quickly and effectively than working alone

Building a network of expertise to draw on can benefit both yourself and others

As mentor

Mentoring is voluntary but extremely rewarding, and can benefit your own skills development and career progression

You need to be the sort of person who wants others to succeed, and have or can develop the skills needed to support them

- Published in Articles

Ways Your Business Can Get Involved In Charity Work

A growing number of businesses are discovering their philanthropic side and are using their financial success to give back to those in need. Here are just five ways in which your business can get involved in charity work.

Donate some of your profits to a cause

The most straightforward way of giving to charity is to donate some of your company profits. You could donate a percentage of your profits on a monthly basis or you could donate sums of money as and when you feel like it. Donations could go to an existing charity or you could create your own charity from which you then direct the proceeds to a cause of your choice.

Launch a fundraising event

Another means of getting involved in charity work could be to launch your very own fundraising event. This could be anything from a fete to a mountain climb. All profits or sponsorship fees from this event can then be donated to a charitable cause of your choice. This is a more hands-on and slightly more complicated form of donating – you may want to get help from services such as Globalfaces Direct to keep track of donors and funds. Whilst more complex, it can be better suited if you yourself don’t have the funds available, plus an event can often attract more media attention and could help you make more of a name for your cause and your brand.

Place a collection jar in your workplace

A simpler way of getting involved in charity work could be to place a collection jar in your workplace for employees or clients to donate money to. You could create a condition to help encourage people to donate such as a swear jar for employees. Once the jar gets full you can then take it to the bank and transfer the cash collected to the cause of your choice. You can buy collection boxes online from companies such as ECL Plastics.

Offer your service/product for free to a cause

It’s possible that you may be able to offer a product or service for free as a charitable gesture. If you’re a catering company, this could include giving free food to the homeless. If you’re a personal trainer, you could offer a month’s worth of free training as a prize in a charity raffle. Doing this could be free marketing for your company as well as contributing to a cause.

Donate equipment to a cause

You may have equipment in your workplace that you no longer need and that you could donate to charity. This could be donated to a charity shop or directly to someone in need. Consider equipment such as old computers, chairs, desks and books that are likely to carry some value.

- Published in News

Why Donations to Charity are Important

Charitable organizations exist to support and raise funds for a specific group of people. There are numerous charities that support a wide variety of causes such as children in various locations, sufferers of various diseases, homeless people and disadvantaged people at home and overseas. These organizations depend on the generosity of the general community to make donations to charity of money, goods and services, in order that they can carry out their work. Many charities are completely self-funded while others receive some government funding.

Throughout history, money has been donated to the needy, as well as food, clothing, tools, bedding etc. These donations were often organized through the Church and it was considered the duty of the wealthier classes and merchants to give to the poor. These days, this generous attitude to giving to the needy is not so well defined. People don’t know how to help or how to make sure their donation goes towards the cause and not just to charity operating expenses.

Why is it important that we donate to charity? Here are just 5 good reasons:

- Help other people – there are millions of people in the world who are worse of than we are at any one time. Many of these folk have problems that are not their fault or are beyond their ability to prevent or change. Humans are a social animal and the best way for mankind to advance is by helping those who are unable to help themselves. We have a responsibility to care for other people, to help those less fortunate than ourselves. When we have some spare cash, time or goods, it is an opportunity to help out.

- Make a difference – donating to charity is the perfect opportunity to make a difference in the world. By making a difference to someone’s life, you are leaving behind a legacy. You are making a statement that your life was worthwhile because you made a contribution to society.

- Feel good – medical and scientific research has proven beyond doubt that giving to other people makes you feel good. The feeling of satisfaction you get when you help someone else is hard to replicate with any other type of activity or endeavor. People who give feel happier, are less anxious and suffer less depression than those who don’t. Better health is enjoyed by those who donate their time, expertise or money to others who are in need. Charitable people tend to be able to cope with their own problems more easily than those who don’t donate. Giving to others improves your self-esteem, self confidence and self worth. This advantage flows into all areas of your life so you will find that you are more confident at work and in social situations.

- Support a cause you believe in – different charities touch the heart of different people. If you are passionate about something or believe that a certain area is important, you will be able to support that cause by donating to charity. You might be passionate about every child having access to a good education; that nobody should live in poverty in the 21st century; that everyone should be able to experience music or art. Whatever you believe in or are passionate about, you will be able to further the cause through donations to charity.

- Meet new people – donations to charity give you the opportunity to met new people and expand your circle of acquaintances. This is especially true when you donate your time or expertise to a worthy cause. While most charitable organizations always need money, many could not operate without an army of volunteers. Whether you give up your time one day a week to serve meals, give a few hours a day to sit with the elderly or travel overseas to help build houses, you will certainly meet many like-minded people along the way. As well as being potential friends, who knows where these new relationships will take you and how these new people might be able to help you in the future?

So shed any doubts you have about why donations to charity are so important and offer your time or money to a cause you believe in. Many other people will benefit but you will also benefit in so many ways.

So, is giving to charity important in your life? What kinds of things do you do to make a difference for others?

- Published in News

5 Reasons Why You Should Donate to Charity

When you choose to give, you may not realize that donating to charity will do more than just help your favourite cause, giving can also provide you with many personal benefits. Whether you choose to donate to charities supporting people living in poverty, advocating to protect the environment, helping animals in need, or addressing other global or local problems, charities need your help to continue their selfless initiatives, but giving can feel just as good as receiving!

Why do people donate to charity? Check out our list of reasons below:

Teach kids the importance of giving.

Teaching children to care about others is an important life lesson. When children watch you give, they will grow up knowing that giving back is the right thing to do and follow in your footsteps. So, donating to charity also helps you be a good role model for your kids.Looking for ways to get kids involved in giving? Read our 20 ideas to get kids fundraising at home, school, and in your community.

Giving promotes feelings of happiness.

Helping others feels good. When you donate to a charity that is important to you, you not only help them continue their vital work, you’re also improving your emotional wellbeing, a win-win situation!

Experience lifelong benefits when you donate your time.

If you are not in a position to contribute financially to charity, but are looking for other ways to give back, considering volunteering your time instead. You will meet new, like-minded people, learn new skills to add to your resume, or complete necessary community hours for school programs.You can also get involved in the community that supports your favourite cause. For example, if you attend a fundraising event for your favourite charity, you’ll meet new, like minded people who care about the same cause.

Donating gives you the opportunity to show gratitude.Life is busy, and it can sometimes be easy to forget to show your gratitude for all that you’ve been given. There are thousands of Canadian charities and causes doing vital work across the country and around the world. When you are ready to give and are researching a charity to support, this can remind us of all that we have, and the act of donating to charity is a way to express our feelings gratitude. Inspire others to give by posting your kind action on social media to inspire others to give generously.

- Published in Articles

Starting A Successful Small Business

Write a business plan, any business plan

You have a passion, and you’d like to make it your profession. No matter how enthusiastic you are about your small business, though, it won’t be successful unless you have a plan in place for how you’re going to start and run it.

It doesn’t matter how long or detailed your plan is, as long as it covers a few essential points. Most successful small businesses will need to have a break-even analysis, a profit-loss forecast and a cash-flow analysis. A cash-flow analysis is especially important since you could be selling your products like hotcakes, but if you won’t be paid for six months, you could still run out of money and have to close your doors.

A business plan is essential because it allows you to experiment with the strategy for your business on paper, before you start playing for keeps.

Determine how you’ll make a profit

Profit is, after all, the ultimate goal of any successful small business. You should examine your business’ expenses (rent, materials, employee compensation, etc.) and then figure out how much you will need to sell to cover those costs and start generating a profit. This is known as a break-even analysis.

Start with as much of your own money as possible

Many small business owners cover their start-up costs entirely through loans, with the expectation that they will begin paying back the loans with the profits from their new business. New businesses can take months or years to generate a profit, however, and loan payments can really become a millstone around the neck of a fledgling operation.

If you can save up as much of the start-up capital yourself before you open your doors, you will help ensure that loans won’t sink your new business. Remember, also, that there’s an outside chance that a lender will call a loan or add unfavorable terms if your business isn’t as successful as you initially planned. If you provide as much of the start-up money as possible, it will lessen the odds of a nasty surprise like this hindering your business.

Protect yourself

Most small businesses are sole proprietorships or partnerships. While these types of businesses are nice and easy to form, they also expose their owners to liability for business debts and judgments. Creditors and judgment holders can come after the owners’ personal assets, like savings accounts and homes, once the business’ money is depleted.

Start small

Everyone wants their small business to be successful, with multiple locations, lots of employees and loads of revenue, but you have to learn to walk before you can run. Don’t spread yourself too thin or take on too many expenses at the beginning, especially if your income might take a while to catch up to your ambitions.

By starting small, you ensure that you can survive the inevitable hiccups associated with running a small business. Those entrepreneurs who begin with modest operations can recover and learn from their mistakes without taking on a lot of debt. Starting small will help your small business grow into a successful enterprise.

Get it in writing

While, it’s nice to do business with a handshake, there’s no substitute for a well-written contract. Indeed, many contracts are not valid unless they are in written form. The exact number of this type of contract varies between states, but here are a few common examples:

- Sales of goods worth more than $500

- Contracts lasting more than a year

- A transfer of ownership in copyrights or real estate

While contracts can be valid when orally made, they are much harder to prove and enforce. Make sure you get all agreements in writing — it will save you headaches down the line, and could even save your business.

Keep your edge

There are many ways to gain a competitive edge over other businesses in your industry: you could have a better product, a more efficient manufacturing or distribution process, a more convenient location, better customer service, or a better understanding of the changing marketplace.

The best way to hold onto your competitive edge is to protect your trade secrets. A trade secret is that information that isn’t known to others that gives you a competitive advantage in the market. There are many kinds of trade secrets, and trade secrets receive legal protection as long as their owners take steps to keep them secret. Those steps could be anything from marking confidential documents to requiring partners and employees to sign nondisclosure agreements.

Another way to hold onto your competitive edge is to stay proactive. If you know that your business is going to face challenges or encroachment by a competitor, don’t wait to react — plan ahead and you’ll stay ahead.

Hire the right people

Don’t just hire the first person to come along with the basic qualifications you need. Look for someone with motivation, creativity and the right kind of personality to make it in your industry and fit in with your business. Then, once you’ve found that person, treat them well, engage them and make sure that you create the environment that they will thrive and give their all in.

Make sure you create the right kind of employee relationship

Lots of businesses try to save money by hiring people as independent contractors rather than full-time employees. The IRS will impose large penalties on businesses that do not withhold and pay taxes for workers that it considers full-time employees rather than independent contractors. Here are some things the IRS will look at to determine whether a worker is an independent contractor or a full-time employee:

- The worker performs tasks that are essential for your business

- The worker only works for your business

- The worker works 40 hours a week, or nearly 40 hours

- The worker receives instructions and training from you, and you exercise control over how the worker does their job

Also be sure to create an “at-will” relationship with your employees. Employers can terminate at-will employees for any reason, which is essential if an employee isn’t working out. There are many ways to make it clear that the employment relationship is at-will, including in employee handbooks and through offer letters. Don’t make any promises to employees about the length or terms of their employment, as these could become binding on you later.

Pay your bills and taxes on time

It should go without saying, but it’s important to pay what you owe — .

It’s also important to pay your regular debts in a timely fashion. If you get a reputation for stalling on a debt, you could find it difficult to form business relationships in the future. Plus, if you stay current on your debts and pay them as you incur them, it will help you avoid being overwhelmed by cash flow problems if several debts come due simultaneously.

- Published in News

Coaching & Mentoring

What are Coaching and Mentoring?

Everything you ever wanted to know about coaching and mentoring

Both coaching and mentoring are processes that enable both individual and corporate clients to achieve their full potential.

Coaching and mentoring share many similarities so it makes sense to outline the common things coaches and mentors do whether the services are offered in a paid (professional) or unpaid (philanthropic) role.

- Facilitate the exploration of needs, motivations, desires, skills and thought processes to assist the individual in making real, lasting change.

- Use questioning techniques to facilitate client’s own thought processes in order to identify solutions and actions rather than takes a wholly directive approach

- Support the client in setting appropriate goals and methods of assessing progress in relation to these goals

- Observe, listen and ask questions to understand the client’s situation

- Creatively apply tools and techniques which may include one-to-one training, facilitating, counselling & networking.

- Encourage a commitment to action and the development of lasting personal growth & change.

- Maintain unconditional positive regard for the client, which means that the coach is at all times supportive and non-judgemental of the client, their views, lifestyle and aspirations.

- Ensure that clients develop personal competencies and do not develop unhealthy dependencies on the coaching or mentoring relationship.

- Evaluate the outcomes of the process, using objective measures wherever possible to ensure the relationship is successful and the client is achieving their personal goals.

- Encourage clients to continually improve competencies and to develop new developmental alliances where necessary to achieve their goals.

- Work within their area of personal competence.

- Possess qualifications and experience in the areas that skills-transfer coaching is offered.

- Manage the relationship to ensure the client receives the appropriate level of service and that programmes are neither too short, nor too long.

Useful definitions

The common thread uniting all types of coaching & mentoring is that these services offer a vehicle for analysis, reflection and action that ultimately enable the client to achieve success in one more areas of their life or work.

- Published in News